It’s only fair. How Explainable AI is transforming compliance

Explainable AI is transforming lending compliance

AI-powered analytics deliver credit risk that is predictive, insightful, and regulation-friendly

BlogPost 19312646446 It’s only fair. How Explainable AI is transforming compliance

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

linear model,

interpretable results,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

Adverse Actions,

credit screening,

Explainable AI,

predictive analytics,

CFPB,

near prime,

FCRA Compliant,

Credit Reporting,

Credit Reporting Agency,

credit decisions,

compliance,

AI-Powered Analytics

Giving traditional credit scores a serious turbo charge

Accept more creditworthy customers with the scored applicants you have already rejected, and identify millions of un-scored and thin-file consumers

BlogPost 19308904324 Giving traditional credit scores a serious turbo charge

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

Artificial Intelligence,

linear model,

interpretable results,

Credit Risk Web Service,

Credit Risk,

Adverse Actions,

Credit Scores,

credit screening,

Explainable AI,

predictive analytics,

CFPB,

near prime,

FCRA,

thin-file,

un-scored,

FCRA Compliant

Ai Lift is giving credit risk a new angle.

AI-powered analytics “bend the curve” to reveal the creditworthy customers you’ve been missing.

BlogPost 17264126124 Ai Lift is giving credit risk a new angle.

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

Artificial Intelligence,

linear model,

interpretable results,

Credit Risk Web Service,

Credit Risk,

Adverse Actions,

Explainable AI,

predictive analytics,

CFPB,

near prime

It’s only fair. Predictive analytics is a win/win for both borrowers and lenders.

New CFPB study shows AI and machine learning can approve significantly more applications, while yielding lower average APRs; Accelitas AI Lift proves itself twice as predictive as the competition. In a recent data test of 18 competitive credit screening scores, AI Lift from Accelitas delivered twice the predictive lift over the vendor average — at 77% the cost of our nearest competitor. By identifying more good customers, AI Lift’s advanced analytics can deliver a ROI of 30:1, creating a win/win scenario for everyone.

BlogPost 12247756602 It’s only fair. Predictive analytics is a win/win for both borrowers and lenders.

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

Artificial Intelligence,

linear model,

interpretable results,

Credit Risk Web Service,

Credit Risk,

Adverse Actions,

Explainable AI,

predictive analytics,

CFPB,

near prime,

FCRA

How to weather the latest lending forecast: Let a Microclimate™ credit score guide you.

Micro-Climate credit scores are becoming the guiding principle for how to weather and navigate the current lending landscape. With the use of Accelitas's AI Life tool, an AI-powered Credit Risk Web Service, it is changing the way lenders are looking at their current landscape and access new borrowers.

BlogPost 11809142687 How to weather the latest lending forecast: Let a Microclimate™ credit score guide you.

Tags:

Machine Learning,

lending,

data waterfall,

Artificial Intelligence,

linear model,

interpretable results,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

Credit Scores,

credit screening,

predictive analytics,

Alternative Lending,

micro-climate score

What does traditional credit screening miss? Start with 70 million potential customers.

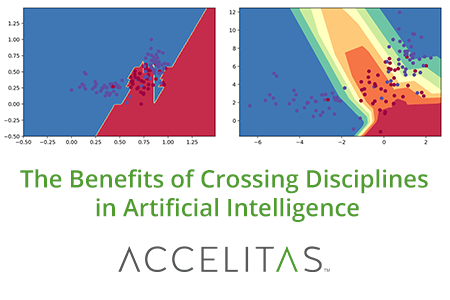

AI includes disciplines such as applied statistics, data mining, pattern recognition, machine learning, deep learning, probabilistic methods, and big data. When applying AI to solve a problem, it is often beneficial to leverage techniques from more than one of these disciplines and sub-disciplines.

BlogPost 11806683277 What does traditional credit screening miss? Start with 70 million potential customers.

Tags:

Machine Learning,

lending,

Artificial Intelligence,

linear model,

interpretable results,

Alternative Data,

Credit Risk,

Credit Scores,

credit screening,

Millennials,

Gen Z,

Alternative Lending,

Credit Invisible

The Benefits of Crossing Disciplines in Artificial Intelligence

AI includes disciplines such as applied statistics, data mining, pattern recognition, machine learning, deep learning, probabilistic methods, and big data. When applying AI to solve a problem, it is often beneficial to leverage techniques from more than one of these disciplines and sub-disciplines.

BlogPost 5709451706 The Benefits of Crossing Disciplines in Artificial Intelligence

Tags:

Machine Learning,

lending,

Artificial Intelligence,

linear model,

interpretable results