What happens when Bank Account validation goes above and beyond?

The Nacha Web Debit Rule is becoming mandatory and enforceable in March 2022. Accelitas keeps you compliant without sacrificing a frictionless account validation experience.

BlogPost 52297416843 What happens when Bank Account validation goes above and beyond?

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers

Sometimes it really pays to follow the rules.

The Nacha Web Debit Rule is becoming mandatory and enforceable in March 2022. Accelitas keeps you compliant without sacrificing a frictionless account validation experience.

BlogPost 52301447831 Sometimes it really pays to follow the rules.

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers

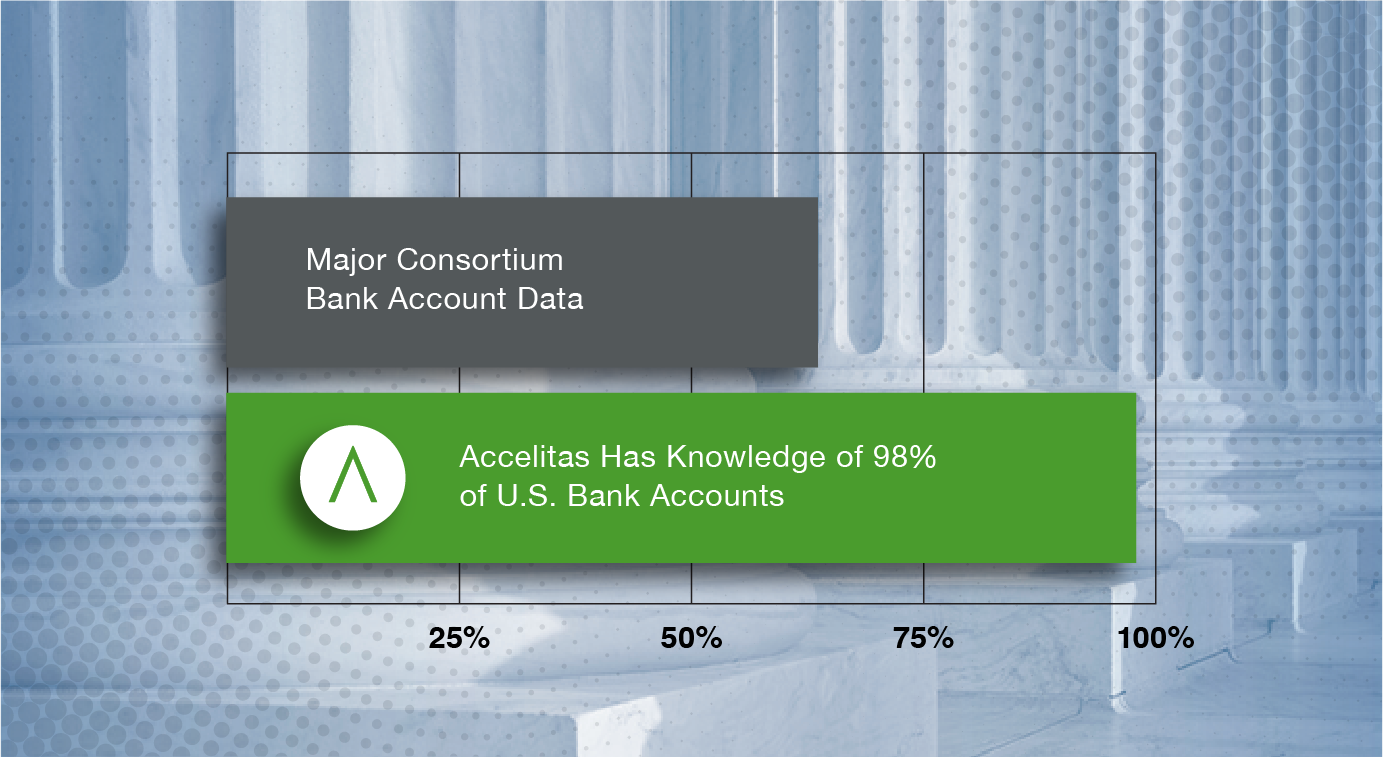

Putting bank validation services to the test? You may be in for a surprise.

If your business relies on rapid online transactions, then you must rely on bank account validations as well. You might be surprised to learn that major account validation services miss up to 30% of accounts. Learn more.

BlogPost 52301447997 Putting bank validation services to the test? You may be in for a surprise.

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers

Microclimate™ credit scores deliver a timely alternative to traditional credit scoring

Accelitas created the Microclimate™ Credit Score – alternative data that allows lenders to find previously rejected but creditworthy applicants. Learn more!

BlogPost 34182693124 Microclimate Credit Scores | Alternative Lending | Ai Lift | Accelitas

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers,

Microclimate Score

Creditworthiness and Lending Decisions take a new turn in 2020

Learn how Accelitas has identified a game-changing opportunity. View this live webinar on the creditworthiness and lending decisions of companies during a crisis.

BlogPost 34182693076 Creditworthiness in Lending | Ai Lift | Accelitas

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers

As fintech seeks next level solutions, Accelitas expands its innovative leadership

Steve Krawczyk named Chief Technology Officer, James Cook brings strategic experience as new Senior Director of Product Management

BlogPost 35305848779 Accelitas | Announcement | Steve Krawczyk | James Cook

Tags:

lending,

Financial Services,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk,

credit screening,

Explainable AI,

predictive analytics,

Credit Reporting,

credit decisions,

AI-Powered Analytics,

Real-time Data,

Creditworthy Borrowers,

Financial Access,

AI,

Predict Credit,

Fintech,

Reimagining Financial Access,

Confirm Identity,

Payments,

Enable Payments,

James Cook,

Fraud Prevention,

Microclimate Score,

CTO,

Steve Krawczyk

Now more than ever: Time to reimagine financial access

Whether serving the needs of borrowers, helping lenders make better credit decisions there’s a smarter way to move forward leveraging technology to reimagine financial access.

BlogPost 29315009294 Reimagine Financial Access | AI | Data | Fintech | Accelitas

Tags:

Machine Learning,

lending,

Financial Services,

Identity verification,

Accelitas,

credit risk management,

Artificial Intelligence,

interpretable results,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

Credit Invisible,

Credit Reporting,

credit decisions,

AI-Powered Analytics,

Real-time Data,

Creditworthy Borrowers,

Financial Access,

AI,

Predict Credit,

Fintech,

Reimagining Financial Access,

Confirm Identity,

Payments,

Enable Payments

Lending during a crisis: the results are in

Since the beginning of the COVID-19 pandemic, Accelitas has been pursuing solutions to help both borrowers and lenders. Learn how analytics is playing a role!

BlogPost 34182317881 Lending During a Crisis | Webinar | Ai Lift | Accelitas

Tags:

Machine Learning,

lending,

AI Lift,

Accelitas,

credit risk management,

Artificial Intelligence,

Alternative Data,

Credit Risk Web Service,

Credit Risk,

credit screening,

predictive analytics,

credit decisions,

AI-Powered Analytics,

Automated Lending,

point-of-sale data,

custom credit score,

COVID-19,

Real-time Data,

Coronavirus,

Essential Retail Transactions,

Creditworthy Borrowers