Unhappy returns: the hidden cost of unsuccessful ACH transactions

Discover how Ai Validate BD eliminates R03/R04 return codes, reduces payment friction, and improves customer experience through smarter, real-time bank account validation.

BlogPost 191311816535 Unhappy returns: the hidden cost of unsuccessful ACH transactions

Tags:

Identity verification,

Bank Account Verification,

Account Validation,

ACH,

Account Verification,

bank account validation,

ai validate

Different businesses have different ACH pain points. That’s why one bank account validation service makes sense.

Discover the five most common pain points in bank account validation—and how Ai Validate BD from Accelitas solves them with real-time, automated ACH solutions. Improve customer experience, reduce costs, and eliminate unnecessary returns across payroll, lending, fintech, and more.

BlogPost 190205894743 Different businesses have different ACH pain points. That’s why one bank account validation service makes sense.

Tags:

Identity verification,

Bank Account Verification,

Account Validation,

ACH,

Account Verification,

bank account validation,

ai validate

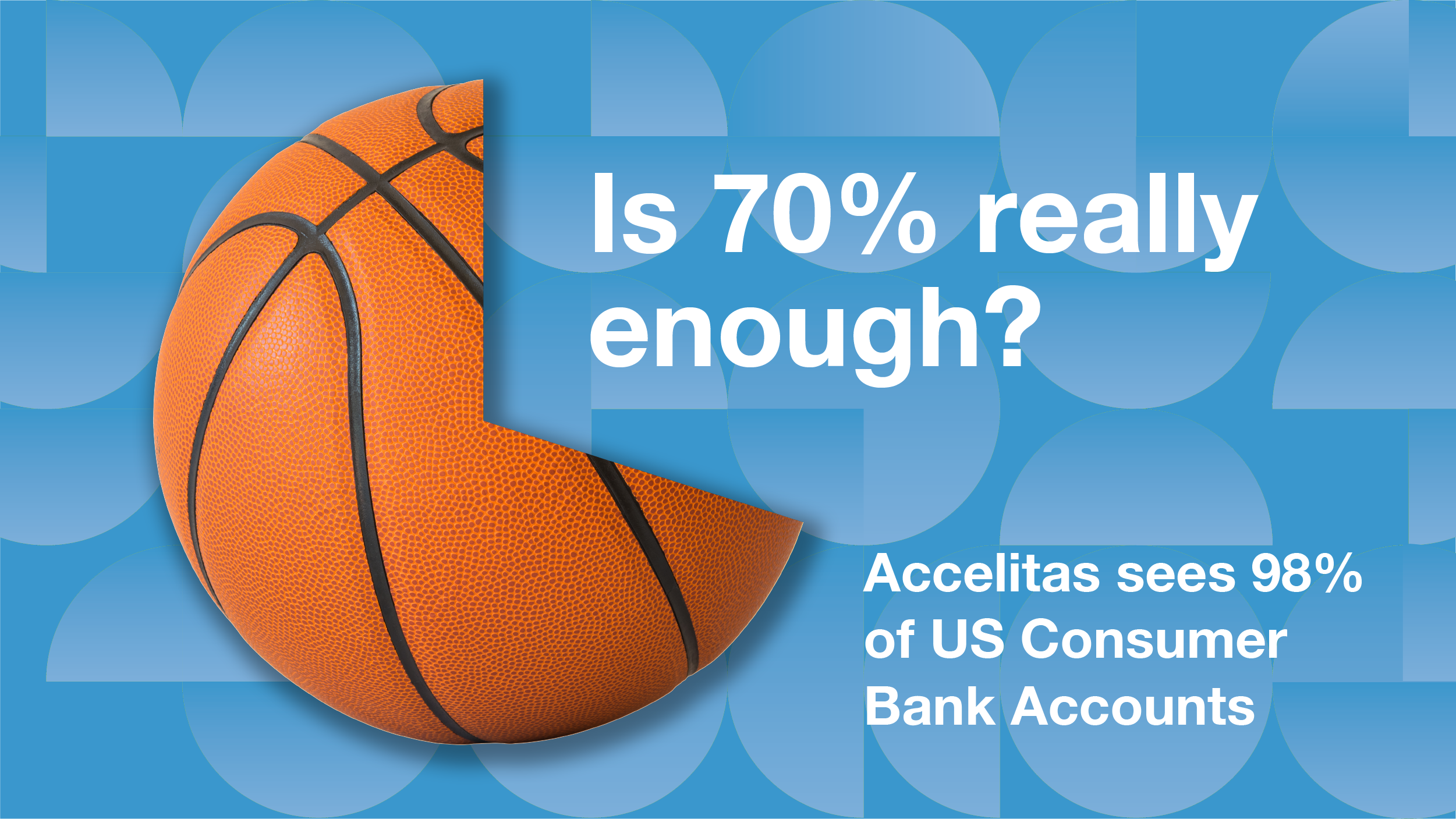

Massive Volume & Missed Opportunity

Learn why outdated bank account validation could be costing your business significant time and money. Accelitas Ai Validate BD provides comprehensive ACH validation, boosting efficiency, ROI, and customer satisfaction. Request your free data test today!

BlogPost 188634693430 Massive Volume & Missed Opportunity

Tags:

Identity verification,

Bank Account Verification,

Account Validation,

ACH,

Account Verification,

bank account validation,

ai validate

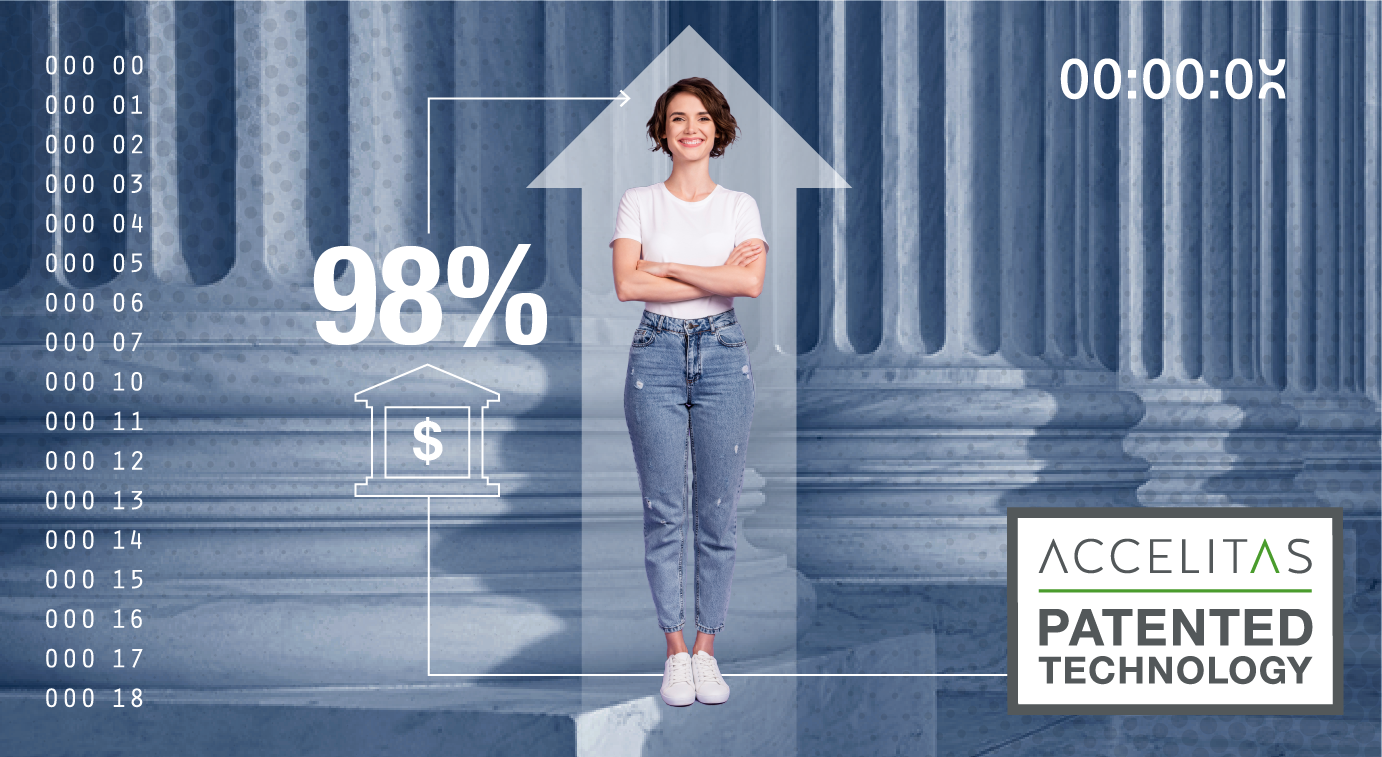

It’s time to find out what your bank account validation is missing

Discover how Accelitas Ai Validate BD revolutionizes bank account validation, reducing costly ACH returns, improving ROI, and enhancing customer experience. Request your free data test today!

BlogPost 188633400618 It’s time to find out what your bank account validation is missing

Tags:

Identity verification,

Bank Account Verification,

Account Validation,

ACH,

Account Verification,

bank account validation,

ai validate

Webinar Examines “True Breakthrough” in Bank Account Validation

Accelitas and Nacha team up to show how predictive data, real-time insights, and new technologies are reducing admin returns and downstream costs for ACH transactions

BlogPost 183479848719 Webinar Examines “True Breakthrough” in Bank Account Validation

Tags:

Financial Services,

Accelitas,

compliance,

AI-Powered Analytics,

Reimagining Financial Access,

Timely payments,

Ai Resolve,

Bank Account Verification,

Accelerated Insight Platform,

Confidence Score,

Account Confirmation,

NACHA Compliance,

ACH-ability,

NACHA,

Account Validation,

Ai Verify,

Fraud,

ACH,

Fraud Screening,

Account Verification,

SOC Compliant

The Unprecedented Workflow Solution That is Changing the ACH Landscape

Patented process lets Accelitas instantly identify invalid bank routing and account numbers to dramatically reduce costs associated with ACH transactions.

BlogPost 180556050045 The Unprecedented Workflow Solution That is Changing the ACH Landscape

Tags:

Financial Services,

Accelitas,

compliance,

AI-Powered Analytics,

Reimagining Financial Access,

Timely payments,

Ai Resolve,

Bank Account Verification,

Accelerated Insight Platform,

Confidence Score,

Account Confirmation,

NACHA Compliance,

ACH-ability,

NACHA,

Account Validation,

Ai Verify,

Fraud,

ACH,

Fraud Screening,

Account Verification,

SOC Compliant

Consider the source: how combining unique expertise generates smarter credit decisions

Discover how Accelitas and DataX, an Equifax company, harness alternative data and custom optimization to enhance credit scoring accuracy and conversion rates. Find out how these fintech leaders are redefining risk management and uncovering profitable opportunities.

BlogPost 167986341975 Consider the source: how combining unique expertise generates smarter credit decisions

Tags:

Financial Services,

Accelitas,

compliance,

AI-Powered Analytics,

Reimagining Financial Access,

Timely payments,

Ai Resolve,

Bank Account Verification,

Accelerated Insight Platform,

Confidence Score,

Account Confirmation,

NACHA Compliance,

ACH-ability,

NACHA,

Account Validation,

Ai Verify,

Fraud,

ACH,

Fraud Screening,

Account Verification,

SOC Compliant

Time for Some Serious Validation

Delve into the critical world of Bank Account Validation (BAV) within today’s rapid transaction landscape. Ensure your BAV solution meets Nacha compliance standards, empowering your business to thrive in the ever-evolving digital marketplace.

BlogPost 166100044039 Time for Some Serious Validation

Tags:

Financial Services,

Accelitas,

compliance,

AI-Powered Analytics,

Reimagining Financial Access,

Timely payments,

Ai Resolve,

Bank Account Verification,

Accelerated Insight Platform,

Confidence Score,

Account Confirmation,

NACHA Compliance,

ACH-ability,

NACHA,

Account Validation,

Ai Verify,

Fraud,

ACH,

Fraud Screening,

Account Verification,

SOC Compliant