Billions of online transactions drive profits and revenue.

“Pay-by-bank” or ACH payments have grown tremendously in every segment. So why are businesses ignoring their Bank Account Validation (BAV) performance?

More than 6 million people are shopping online at this moment and are likely to purchase more than 300,000 items before you finish reading this. Just as remarkable as the speed and volume of today’s digital transactions is the fact that we now take them for granted.

The good news is that businesses have systems in place to monitor things like ACH transactions.

The bad news is that some of these systems are wildly ineffective.

The confusing news is that many businesses don’t know this because they don’t measure their Bank Account Validation (BAV) performance at all.

Having checked the mandatory box for Nacha compliance, few consider BAV part of their business strategy.

And that’s a lot to overlook. You could be losing business to skilled fraudsters or impatient millennials and not know the difference. You could be ignoring a simple solution to lowering your cost of payment acceptance and avoiding more expensive payment options. You might be missing valuable new business because your current BAV process is rejecting perfectly good customers.

How does something so crucial to today’s commerce get so little attention?

A quick look at how we got here

Many Americans got their first taste of the online payment ecosystem using ACH in the early days of the internet, often on eBay. Buyers and sellers both needed assurances and with the help of micro-deposits — those “penny or two” test runs for the actual purchase — you could verify a working bank account in as little as 48 hours. Since it was the only way to do it, everyone did it and no one complained. Most were happy to let PayPal handle the process for them. In hindsight, of course, those 2 or 3 days to complete the validation, ran counter to the promise of internet commerce.

Soon, merchants began adopting their own online acceptance procedures. Like their brick-and-mortar counterparts, credit cards became the dominant currency. The 16-digit primary account number didn’t lend itself well to manual entry, risk levels remained problematic, and the interchange costs proved considerably more expensive than ACH transactions.

So online vendors rediscovered an old standby – the personal check – with account and routing numbers updated digitally through providers like TeleCheck. PayPal became a true payment wallet, allowing businesses to outsource the coding and reduce friction for consumers. Pretty soon every payment option seen at the physical point-of-sale was brought to the internet… credit cards, debit cards, gift cards, and coupons.

The more things change, the more problematic it gets

Meanwhile, banks had a clear and vested interest in bank account validation and recognized the value of their bank data. Some of the largest banks got together to form a network - Early Warning – but their data was not complete or necessarily robust, and over time they substantially restricted its access.

And all this time the new generation of consumers were changing their spending habits and credit profiles faster than the internet could track. Especially if merchants weren’t paying attention in the first place.

It turns out that while online payment protocols have evolved, it hasn’t been a linear progression. Merchants and billers farm BAV out to vendors, or concoct their own system, but rarely attempt to improve the process. ACH still works at a much lower cost than credit cards, but there are a lot of different flavors of ACH to choose from. And many of those 1990s bank acceptance hurdles still exist. While one bank data source might be fine for Client A, it could be disastrous for Client B.

Enter data science: BAV goes real-time

For Accelitas, BAV actually was a linear progression. We’re a data analytics company that likes to work with customers on new business-specific solutions. We learned long ago that one size does not fit all, and BAV has become considerably more complex than traditional yes or no analytics. Every business has a different threat matrix -often with multiple use cases - and enriching the data with non-credentialed sources and machine learning helps you make better decisions across transaction scenarios.

Measuring for performance should be part of the process, but even people who run very smart businesses may not sit down and analyze their BAV services. When they learn how ineffective the process really is, some are even appalled. They may find themselves saying “no” and “yes” to the wrong people and paying for an authorization that’s no good. They don’t know if they lost a customer or remediated them. They aren’t tracking the tremendous number of downstream costs and risks.

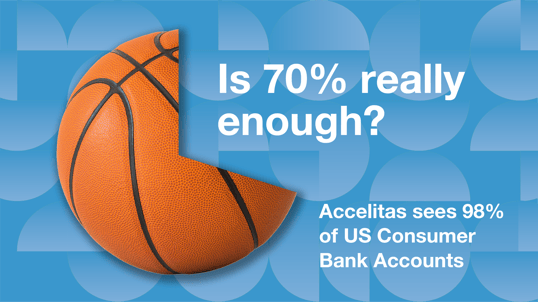

Our job is to look at bank account data and predict things. We’ve gotten very good at it. So good that we’ve patented a revolutionary process to tackle Nacha R03 and R04 returns in a way that no one else has. With unmatched coverage of U.S. bank accounts and real-time data updates, Accelitas is doing what the traditional players can’t — delivering instant bank account validation tuned to your specific business needs. That means you can reduce fraud and abandonment rates, meet Nacha requirements, and grow your business. You don’t even have to find new customers. Just serve the customers already coming your way.

A lot has changed in the payments space. And a lot hasn’t. But one constant always rings true: you still have to pay attention.

Learn more about BAV and how you can elevate your business’s financial security and efficiency.